Target profit is the desired profit that a business wants to achieve in an accounting or manufacturing period. The conventional approach is to set budgets and compare results against standards.

A comprehensive approach to follow is the cost-volume-profit analysis. The target profit calculation is an integral part of the CVP analysis.

Let us discuss this desired profit concept and different methods to calculate it.

What is Target Profit?

Target profit is defined as the expected amount of profit that a business intends to achieve during a specified accounting period.

A common approach to achieving this desired profit is through the budgeting process. The management can set a target to achieve by the budgeting period end.

It is the amount of revenue that is earned after covering all fixed costs. It means when the business generates revenue beyond the break-even point, it starts earning profits. The management can set a specific amount as target profit above that break-even point.

How to Determine the Target Profit?

A business can set target profit through any method. For instance, a business can set a dollar amount to achieve through increased sales.

However, there are two common approaches adopted by most businesses.

Budgeting Approach

This is the common approach taken by many small and medium businesses. The management sets budgets for sales and costs to achieve a target profit. Achieving profit requires controlling costs and achieving budgeted sales through this method.

Variances in budgets are common. However, many businesses fail to achieve it through this approach as they cannot control budgets.

The CVP Approach

Since budgets come with inevitable variances, an alternative method is desired. An alternative method is to follow the cost-volume-profit or the CVP approach.

The CVP method can be used to first determine the break-even point. At this point, the company will earn sufficient revenue to cover all the fixed costs.

The management can then add the desired profit that comes through excess of the break-even point sales.

Target Profit Calculation Process

It can be calculated using the CVP approach and budgetary methods. The choice largely depends on the complexity and nature of the business.

We’ll outline the preferred CVP method process here.

Determine the Timeframe

The first step is to set a production and target profit timeframe. Without setting time limits the practice of the target profit approach would be futile.

Set Target for the Contribution Margin

The CVP method requires the calculation of contribution margin first. It is the gross profit that is sales minus the variable costs of production.

Calculate Fixed Costs

Next, the CVP method requires determining the fixed costs as well. The fixed cost figure is an important item in the CVP formula.

Apply the Formula

In the final step, all figures are placed in the following formula to calculate this profit.

Sales = (Fixed Costs + Target Profit) / contribution margin per unit

Any adjustments for the variance in the actual and projected results can be adjusted in this final step as well.

Target Profit Calculation Formula

As mentioned earlier, there are several methods to calculate it for a business. The CVP method is an accurate and widely used method that can be used in single or multiple products scenarios effectively.

Here we can take two different approaches to figure out this desired profit.

The Equation Method

The first one is the equation method that uses the basic profit equation. It is useful in scenarios where the management wants to set target profits against total revenue in a particular timeframe.

Profit = Total Revenue – Total Variable Costs – Total Fixed Cost

Or,

Profit = (USP × Q) – (UVC ×Q) – TFC

Unit variable costs and production volume will remain constant and in proportion as the production level changes. The total fixed costs apportioning will change as the volume of production changes.

If the profit is set to zero, the company can achieve the break-even point with the help of this equation. Else, the desired profit amount is set to determine the output quantity or the production volume level.

The Contribution Margin Method

The second method is to first calculate the contribution margin and then set a target profit. The contribution margin is the revenue minus variable costs of production.

The formula is given below:

Required Sales = (Target Profit + Fixed Costs) / Contribution Margin Per Unit

If it is set to zero in the above equation, it will give the break-even point in terms of sales.

The above equation can be used with a little variation of using the C/S ratio instead of the contribution margin.

Required Sales = (Target Profit + Fixed Costs) / C/S Ratio

where,

The C/S ratio = Contribution Margin / Sales.

Target Profit Calculation – Multiple Products

The methods discussed above are useful for a single-product facility or a manufacturing facility with a limited number of products. However, in many cases, there are several similar products manufactured in the same facility.

The management can use the graphical method to calculate the break-even sales points as well as target profits for each product. This method uses the profit-volume relationship to calculate target profit.

The graphical method of the profit-volume analysis assumes that the company must sell its most profitable product first.

The CVP method finds the break-even sales point when the profit is set to zero. Instead of setting the profit to zero, the management can use the desired profit amount and follow the same steps to calculate the desired output quantity.

The graphical method requires a step-by-step approach. Suppose a company ABC sells three products P1, P2, and P3.

Step 01:

The first step is to determine the profitability of each product and rank them accordingly. The C/S ratio is a useful tool to rank products here.

Step 02:

The second step is to draw the graph with the cumulative sales showing on the x-axis and the profit on the y-axis. At the starting point, the graph will show only straight lines.

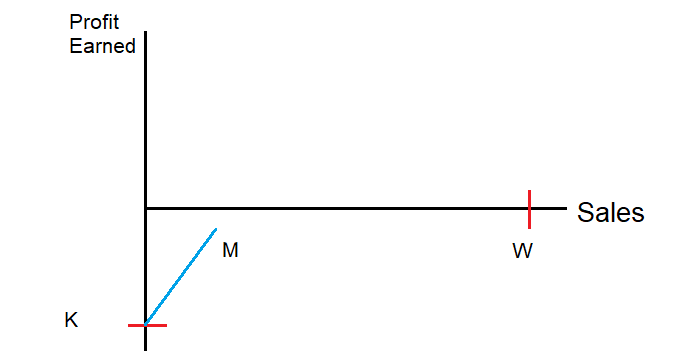

Step 03:

Draw a line that represents the profit of P1 (the highest-ranked C/S product) scaled to the graph on the y-axis.

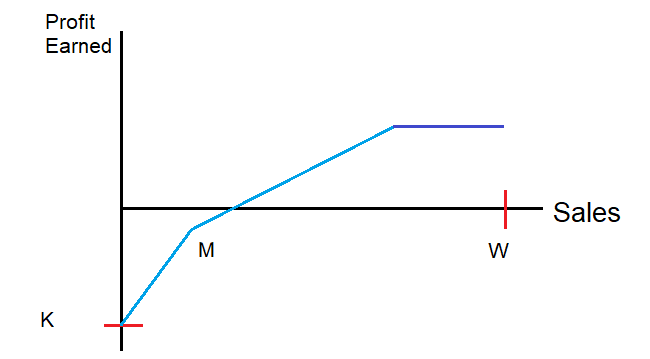

Step 04:

Draw the lines to represent the profits of products P2 and P3 ranked respectively according to the C/S ranking.

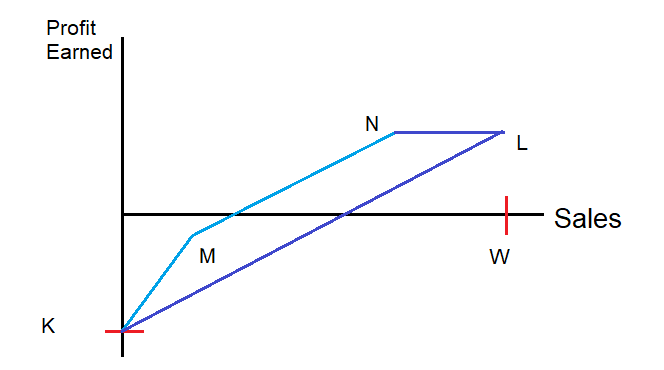

Step 05:

Draw the joining line of the final point L and the first point K on the graph. The point at which it crosses the x-axis represents the break-even point of sales.

If the company ABC had set a target point, the crossing point at the x-axis will represent the required sales to achieve that target profit.

Target Profit Calculation for Multiple Products – Alternative Method

An alternative method using the weighted average cost to sales (C/S) ratio can be used to determine the target profit as well.

The formula to calculate it will be:

Sales Required = (Total Fixed Costs + Target Profit) / Weighted Average C/S Ratio

Again, setting the target profit to zero will give the sales break-even point.

Advantages of Using Target Profit Approach

Target profit and cost-volume-profit analysis combined can offer useful information to the management for decision-making in the long term. It can be seen as part of the wider approach of the CVP analysis.

Here are a few advantages of using the target profit approach as compared to the arbitrary budgeting method.

- It sets quantifiable and clear objectives for a company as well as aligns the financial goals of any business for profit maximization.

- It helps set accurate profit targets that can be achieved through analysis of required revenue at specific volume production.

- This method helps management to control and improve operating efficiency.

- The management can use the analysis for detailed product costing, pricing, and profitability evaluations.

- This method can be used in a single or multiple-product environment.

- Target profits consider both fixed and variable costs of production. Thus, the analysis offers a comprehensive evaluation of the overall operating efficiency of a business.

Disadvantages of Using Target Profit Approach

Despite its usefulness, the target profit approach can offer some disadvantages as well.

- It can be difficult to execute in the multiple-product environment as it will take substantial time and effort.

- Setting desired profits does not ensure success as variances can still occur as is the case with the budgeting approach.

- Evaluating variable and fixed costs along with the required sales figures can be a complex and tangling task.

- Failure to achieve unrealistic target profits can result in employee demotivation.

- The target profit approach relies on the cost-volume method, that in turn, relies on several operating procedures and inputs.

Concluding Remarks

Target profit is an integral part of the cost-volume-profit or the CVP analysis. It helps management set profit targets to increase operational efficiency.

The target profit approach is a useful tool in achieving the financial objectives of the business. It also motivates employees and the management. The target profit method can be used in a single or multiple-product environment. However, it also offers some limitations in the form of variance in results, employee demotivation, and unrealistic approaches from the management.