In the previous article, we have covered the present value of an ordinary annuity. In this article, we cover the present value of an annuity due in detail. This includes the definition, how to calculate it with the example, the present value of an annuity due table as well as the comparison between the present value of an annuity due and ordinary annuity.

So let’s dive in!

What is Present Value of an Annuity Due?

As you might have known, the annuity due refers to the stream of periodic equal cash flow that occurs at the start of each period.

Thus, the present value of an annuity due is the measurement of the current value of future periodic equal cash flow that occurs at the start of each period.

It is used to know how much money now to get the future periodic future cash flow or future returns.

How to Calculate Present Value of an Annuity Due?

In order to calculate the present value of an annuity due, we simply perform the adjustment of an ordinary annuity. This is done by discounting back one less year than the ordinary annuity. This is because the cash flow of an annuity due occurs at the start of each period while the cash flow of an ordinary annuity occurs at the end of each period.

Therefore, we just need to convert the present value interest factors of an ordinary annuity by multiplying by (1+i). By doing this conversion, it means that we effectively add back one year of interest to each annuity cash flow.

We can simply write down the formula of discounting the present value interest factors of an ordinary annuity as follows:

PVIFA (i, n) (annuity due) = PVIFA (i, n) × (1+i)

Where:

PVIFA (i, n) = [1 – (1+i)-n]/i

Thus, we can rewrite the formula as follows:

PVIFA (i, n) (annuity due) = [1 – (1+i)-n]/i × (1+i)

Therefore, the present value of an annuity due formula can be written as follows:

PV of an annuity due = PMT × PVIFA (i, n) (annuity due)

Or PV of an annuity due = PMT × PVIFA (i, n) × (1+i)

Or, we can also rewrite the PV of an annuity due formula on long-form as follows:

PV of an annuity due = PMT × [1 – (1+i)-n]/i × (1+i)

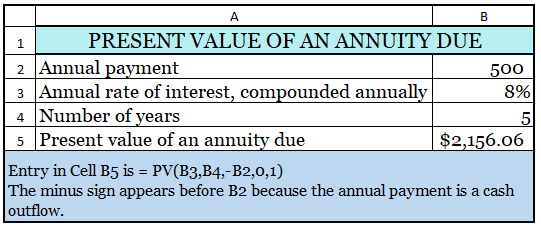

We can also calculate the present value of an annuity due by using Excel spreadsheets. In the later section below, we will illustrate how to calculate the present value of an annuity due by using the formula and the Excel spreadsheets.

So let’s go through the example and calculation together!

Example

Let’s assume that ABC Co is considering choosing an option whether the annuity due or ordinary annuity. ABC Co is considering a stream of periodic equal cash flow of $500 per year for 5 years with a minimum interest of 8%.

Calculate the present value of both annuity due and ordinary annuity. Which one should ABC Co choose?

Solution:

Now, let’s firstly calculate the present value of an ordinary annuity. By using the short method, we can calculate the PV of an ordinary annuity by using the formula below:

PV of an ordinary annuity = PMT × PVIFA (i , n)

Where:

PMT = $500

PVIFA (8%, 5yrs) = 4.329 (From present value of an ordinary annuity table)

Hence, PV of an ordinary annuity = 500 × 3.993 = $1,996.5

Therefore, the present value of an ordinary annuity is $1,996.5.

Next, let’s calculate the present value of an annuity due. This is done by using the below formula:

PV of an annuity due = PMT × PVIFA (i, n) (annuity due)

Where:

PVIFA (8%, 5yrs) (annuity due) = PVIFA (8%, 5yrs) × (1+i) = 3.993 × (1+0.08)

Thus, PVIFA (8%, 5yrs) (annuity due) = 4.3124

Therefore, PV of an annuity due = 500 × 4.3124 = $2,156.2

We can also calculate the PV of an annuity due by using the Excel spreadsheet as below:

You can develop your own Excel spreadsheet calculation by using this sample.

Present Value of an Ordinary Annuity Vs Present Value of an Annuity Due

As mentioned above, the PV of an annuity due is calculated by multiplying the annuity cash flow with the discounted PVIFA of an ordinary annuity. This one of the key differences.

Another difference is the cash flow of each annuity. The annuity due cash flow occurs at the beginning of each period while the ordinary annuity cash flow occurs at the end of each period. This, theatrically, means that the PV of an annuity due will always greater than the PV of an ordinary due.

This can be proof by looking at the example above. The PV of an annuity due is $2,156.06 while the PV of an identical ordinary annuity is only $2,050.10. Thus, the PV of an annuity due is greater than the PV of an ordinary annuity of $105.96.

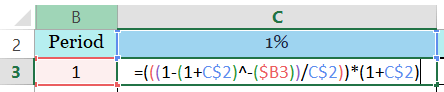

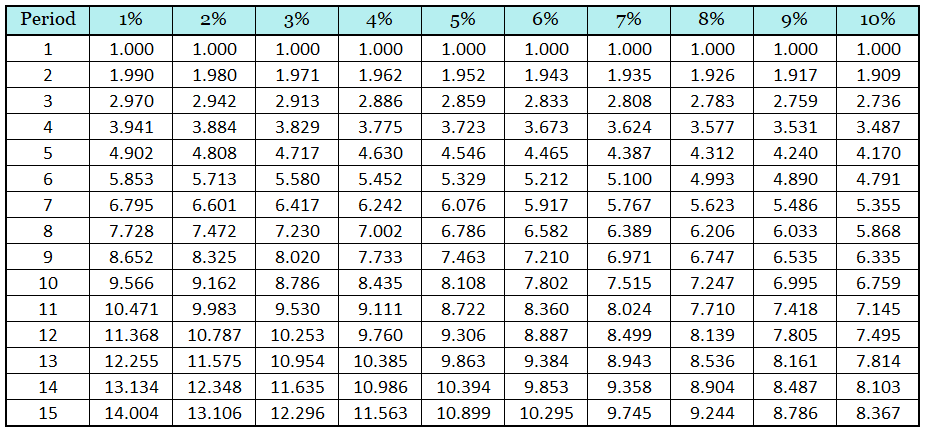

Present Value of an Annuity Due Table

In most finance or corporate finance or financial management book, there is no present value of an annuity due table. In most of the books, they provide only the present value of an ordinary annuity table.

So how can we generate the present value of an annuity due table?

This is simple. You just need to convert the present value interest factors of an ordinary annuity by multiplying with (1+i). This is because an annuity due takes into account the cash flow at the start of each period. Thus, you need to discount back one year of interest to each annuity cash flow.

The formula below is to calculate the present value interest factors of an annuity for year 1 at an interest of 1%. So you get the rest as per the table below, you just need to copy this formula and paste to each of the cells in the table below.

Final Thought

The present value of an annuity due is the current value of the future periodic cash flow occurs at the beginning of each period. The PV of an annuity can be calculated by using the present value of an annuity formula or by using an Excel spreadsheet. The value of the PV of an annuity due is always greater than the PV of an ordinary annuity.