Introduction

In this article, we will cover in detail the Direct Labor Efficiency Variance. Commonly, human capital is called the most precious asset for any organization, skilled labor for manufacturing companies in particular hold an important for efficient manufacturing. For companies producing a large number of different products and utilizing skilled labor, labor efficiency holds an important tool to measure the performance of the manufacturing process as a whole. The total Labor variance consists of two parts:

- The labor rate variance and

- The labor efficiency variance or the direct labor efficiency variance

In this article, we will focus more on the direct labor efficiency variance while the labor rate variance will be covered in another article.

Table of contents

- Introduction

- Definition

- Important of Calculating Direct Labor Efficiency Variance

- Direct Labor Efficiency Variance Formula

- Example Calculation of Direct Labor Efficiency Variance

- Explanation and Analysis

- Advantages of Direct Labor efficiency variance analysis

- Limitations of the direct labor efficiency variance analysis

- Conclusion

Definition

The direct labor efficiency variance is the difference between the standard or budget labor hours allocated and the actual labor hours consumed for the production.

Whereas the labor rate variance is the difference between standard labor cost and the actual labor cost for the production.

The utilization of the labor resources depends on two factors the time taken and the rate per hour paid to the labor. The efficiency of labor is the optimum of labor hours available to the best use of the profit-making products in a product mix. Firms producing more products analyze the product mix variances to achieve the optimum production level where the maximum resources are allocated to the profit-making products, labor hours are often the bottleneck resource in many production units, and so efficient utilization of the labor hours available can maximize the profits. In any manufacturing process, the management may decide to use temporary or hour-based labor in case of direct labor shortage or for the production increment purpose. However, in the long term, direct labor efficiency analysis holds more significance in control measures and performance appraisals.

Important of Calculating Direct Labor Efficiency Variance

The productivity of labor is an important measure for any manufacturing business, variance in standard and actual direct labor hours can provide the management with useful information about the skills level of the labor force. The availability of direct labor hours is often scarce in bulk production so utilizing the labor hours to maximize the profits is important for sales and production targets too.

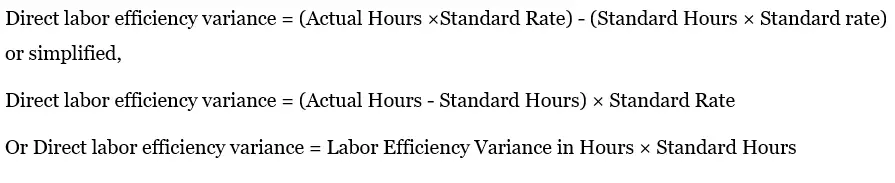

Direct Labor Efficiency Variance Formula

This variance can be calculated as:

Example Calculation of Direct Labor Efficiency Variance

Example 1:

Suppose Techno Blue manufactures 5,000 units of a product P1. The data given for the production cost is as:

| Actual Hours Per Unit | Standard Hours Per unit | Standard Rate Per Hour | |

| Direct Labor cost: | 0.4 | 0.3 | $ 10 |

Require: Calculate the Direct Labor Efficiency Variance for product P1.

Solution:

Based on the formula above, we can calculate the variance as follow:

First, we need to calculate the total actual labor hours as well as the standard labor hours.

So actual hours needed to produce 5,000 units = 5000 × 0.4 = 2,000 Labor hours

Whereas the Standard Hours should be = 5,000 × 0.3 = 1,500 labor hours

Direct Labor efficiency variance = (2,000 – 1,500) × 10

= $ 5,000 ADVERSE

In addition, in order to make the calculation of such variance easy to understand, let’s separate the calculation into 4 steps as follow:

Step 1: Calculate the Actual Hours:

The total actual hours can be calculated as follow:

Actual Hours = Units Produced × Actual Hours per Unit

= 5,000 × 0.4 = 2,000 labor hours

Step 2: Calculate the Standard Hours:

The standard hours should be can be calculated as follow:

Standard Hours = Units Produced × Standard Hours per Unit

= 5,000 × 0.3 = 1,500 labor hours

Step 3: Calculate the Labor Efficiency in Hours:

The labor efficiency in hours is the difference between the total actual hours and standard hours. The total labor actual and standard hours were calculated as per step 1 and step 2 above.

Thus; Labor Efficiency in Hours = 2,000 – 1,500 = 500 hours

Step 4: Calculate the Variance

This is the final step is to calculate the variance.

As per the formula above, we calculate the variance as follow:

Direct Labor Efficiency Variance = Labor Efficiency in Hours × Standard Rate

= 500 hours × 10 = $5,000 ADVERSE

In this simple example, this variance shows ADVERSE variance, because the labor took more hours per unit and cost more per unit than the standard or budgeted targets.

Example 2:

Continuing from example 1:

Let’s assume further that instead of the actual hours per unit of 0.4, Techno Blue manufactures was able to produce at 0.25 actual hours per unit.

Thus the actual labor hours would be as follow:

Actual Hours = Units Produced × Actual Hours per Unit

= 5,000 × 0.25 = 1,250 labor hours

Therefore, the variance would be as follow:

Direct Labor efficiency variance = (1,250 – 1,500) × 10

= $ 2,500 FAVORABLE

Explanation and Analysis

Typically, a favorable direct labor efficiency variance indicates that there is better productivity of labor used in the production. In contrast, an adverse or unfavorable variance shows the inefficiency or low productivity of the labor used in the production.

Reasons for Favorable Variance

Direct labor efficiency variance can be achieved in favorable as:

- Experienced and skilled labor workers

- Continuous process improvements to reduce wastes and improve the production rates

- Training the labor force when new equipment and tools are purchased

- Motivating the production department to adapt the total quality management approach that can significantly improve the production rates

- Eliminating the idle hours, or utilizing the direct labor idle hours for other production processes

Reasons for Adverse or Unfavorable Variance

Many factors that can cause adverse direct labor efficiency variance as follow:

- Low staff motivation levels if there is no incentive for higher productions

- Low skill levels in labor, or unfamiliarity with new machines and tools

- Idle labor hours due to unavailability of raw material or power shortfalls etc.

- Inaccurate standard labor hours set as target labor hours per production unit

As in any variance analysis, the direct labor efficiency variance should also be interpreted realistically. Some of the factors may not be in direct control of the labor force, for example, the idle direct labor hours may be caused due to the unavailability of the raw material or power shortfall, but that can adversely affect such variance. It is wise to further breakdown the direct labor efficiency into the:

A) Productive efficiency variance and

B) Excess idle time variance

This breakdown will identify the cause of change in this variance that in turn can affect the total labor variance. As the labor idle time can cause adverse direct labor efficiency variance the management can take several steps to reduce the idle time:

- Timely supply of raw materials through contracts with reliable suppliers

- Maintenance of machines and production planning ahead of time

- Training direct labor workforce when introducing the new machines

The direct labor or permanent workforce will be paid during the idle labor or machine hours, so the process efficiency in production will get affected adversely.

Advantages of Direct Labor efficiency variance analysis

- It helps management to best utilize one of the most critical resources in production I.e. labor hours

- It helps to identify the actual cause of variance by differentiating in idle work hours and direct labor efficiency variances

- Firms applying TQM or JUST IN TIME (JIT) approaches will keenly observe the direct labor efficiency as it plays a key part in continuous process improvements

- In a product mix, the percentage of profits from different products may vary, so it’s critical to assign maximum resources such as direct labor to the profit-making products

Limitations of the direct labor efficiency variance analysis

There are some limitation regarding this variance analysis as follow:

- The setting of benchmark standard labor hours is difficult as the historic data may become obsolete in fast-paced production facilities

- Studying detail for direct labor rate, direct labor efficiency, and labor idle hours take significant time and skills

- Idle labor hours are often non-relevant to the variance as the factors are often uncontrollable for the labor force

Conclusion

Control cycles need careful monitoring of the standard measures and targets set by the top management. Variance analysis is also an important tool in performance measurement and forecasting for future planning and budgeting.

However, one particular indicator such as direct labor efficiency variance cannot determine the whole process of efficiency or productivity. We commonly see the skilled labor hours as bottleneck measures in various production facilities, so careful analysis for the direct labor efficiency and utilization for the best products can enhance the overall profitability. Such control measures can also motivate the direct labor to work on reducing idle labor hours, process wastes, and inaccuracies that can be a useful starting point in applying the total quality management approach.