Introduction

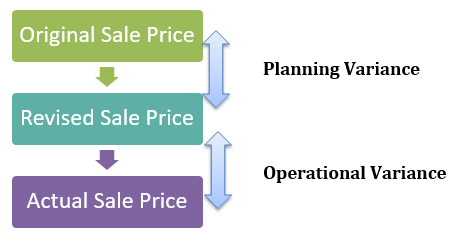

Fast paced and dynamic market conditions mean the companies need to stay alert and responsive to the changes. Product sales pricing is one of the most crucial decisions to stay competitive or take the market leader position. Management performs budgeting and planning activities to set a standard sale price per unit for each product. Operational and manufacturing can cause the costs to change, hence a change in the sale price becomes inevitable. Variance in sales price is the measure of deviation from planned to the revised, and revised to the actual estimates. The variance may occur due to poor planning or lack of plan implementation, unplanned events or unforeseen economic factors.

Definition

“The comparison between the number of product units sold at actual selling price and the budgeted selling price” is called the Sales Price Planning Variance.

Sales Price Planning Variance Formula

Sales price variance may occur due to operational or planning reasons, the general formula to calculate the planning and operational variances is:

The numerical formula to calculate the Sales price planning variance will become:

Working Example

A simple working example for a company selling one product can be described as:

Suppose a company plans to sell 5,000 units of a single product at $ 15 per unit. Due to seasonal demand for the product, the management realized they can charge a higher price for the product at $ 17. That yields a favorable sales price variance as:

Sales Price Planning Variance = (Revised Sales Price – Original Sales Price) × Actual Units Sold

Sales Price Planning Variance = (17 – 15) × 5000 = $ 10,000 Favorable.

The usefulness of this variance comes in a sales mix of products.

Suppose Techno Blue sells 3 products P1, P2 and P3 with the following data:

| Product | Budget Sale Price $ | Revised Sales Price $ | Budget Sale Units | Actual Sales Units |

| P1 | 20 | 15 | 2000 | 1900 |

| P2 | 25 | 30 | 2000 | 2300 |

| P3 | 25 | 27 | 2000 | 2000 |

There can be several reason both internal and external causing a change in the sales price discussed in detail below. The total sales price planning variance for 03 products can be calculated as:

| Product | (Revised Sales Price – Original Sales Price) × Actual Units Sold | Variance in $ | Favorable/Adverse |

| P1 | (15 – 20) × 1900 | 9,500 | Adverse |

| P2 | (30 – 25 ) × 2300 | 11,500 | Favorable |

| P3 | (27-25) × 2000 | 4,000 | Favorable |

| Total Sales Price Planning Variance | $ 6,000 | Favorable |

Analysis and interpretation

There are a number of factors causing a change in the product costs to change. These factors can be planned or unplanned events. A change in the cost of any product will compel the management to change the selling price. The budgeted or standard selling price will need to be revised; the difference in the selling price for actual number of units sold will then give the variance in the sale price planning.

Causes for sales price planning variance include:

- Change in the raw materials prices, compelling management to revise sale prices significantly

- Inefficient operations or unskilled labor, causes the product prices to rise or conversely efficient production to control the costs

- Market competition, with fewer competitors likely to achieve favorable sale price variance and intense competition to result in adverse

- Unrealistic budgeted or standard sale price planning

Sales price planning variance can occur due to internal and external factors for the company. Today’s dynamic and fiercely competitive market demands management to stay alert and respond to the changes quickly. The operational managers should then make sure to achieve the revised budgeted sales prices. The sales price planning variance is a collective responsibility of the cost accountants, operational managers, and the sales and marketing managers.

Why it is important to Calculate the Sales Price Planning Variance?

Competitive and attractive sales price for a product can be the difference between a successful and failed product launch. Also for market leaders, to maintain the market share it is important to keep the variances in check. A well planned sale price can help a company gain competitive advantage in the market.

- Several uncontrolled events cause costs of production to change, revising the budgets keeps the product prices competitive

- This variance provides an overview of manufacturing efficiencies to the management

- It helps to achieve the targeted sales volume

- This variance offers detailed profitability analyses for each product in a sales mix

- It helps management to close gaps in the historical planned budgets and up-to-date market standards

Although the sales price planning variances provide many benefits, some limitations do associate with it:

- Operational and marketing managers may find themselves at odds with sales price variance results

- Uncontrollable factors causing adverse sales price variance can result in lower staff motivation

- The management may not be able to achieve the revised sale prices due to lack of capacity

Conclusion

Total sales variance depends on the sales price and sales volume variances. Often these variances offset each other. Increased revenue is a prime target for any company. The importance of careful sales price planning is unarguable. Measuring numeral values cannot yield positive results for any company.

The best way to utilize the variance and control measure is to analyze the true causes of the variances both in operations and planning. Strategic budgetary planning happens in the beginning of the year, but quarterly and monthly budgets should often be revised. It is a collective responsibility of the operational and marketing department to close the gap between revised sales price and original sale price planned. An efficient marketing department in collaboration with operational team can maximize the advantages in case there are fewer competitive products. On the hand, the sales price planning variance can help a company stay competitive in the market in case of fierce competition.